In collaboration with

"Suljhao magar pyaar se"

*Online Dispute Resolution is a method of resolving conflicts outside of the traditional courtroom to reach mutually agreeable solutions.

Timeline

7 weeks

Design Research Intern with a team of three as a part of an academic project.

Team & Role :

*

Online Dispute Resolution

Reimagining

To tackle

Loan defaults

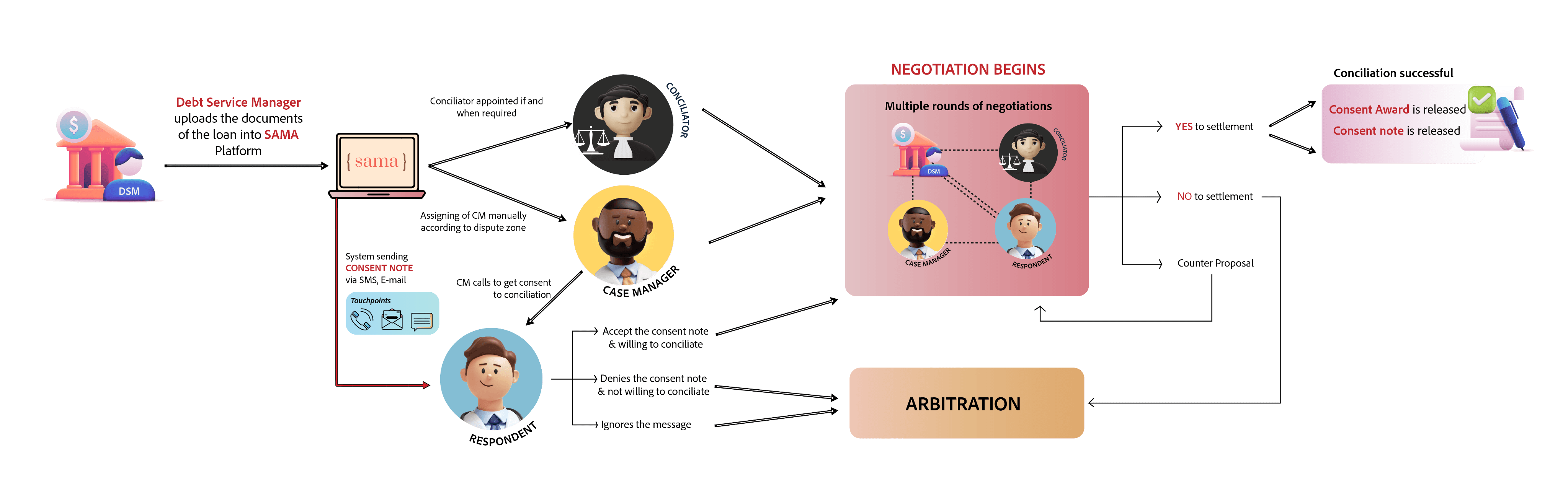

This design research project focuses on providing insights on the settlement behaviour patterns of loan defaulters within the context of an online dispute resolution platform named SAMA. Areas of intervention and process optimisation strategies were suggested to SAMA to increase the settlement rate of the platform through conciliation (a method of ODR)

Introduction:

In recent years, the issue of loan defaults has become a pressing concern in India's financial landscape. The increasing number of default cases puts immense pressure on both lenders and borrowers, leading to prolonged legal battles, financial burdens, and strained relationships. Recognising the need for a more efficient and humane process, alternate dispute resolution methods like conciliation have gained prominence as viable solutions.

Quantitative Data Analysis-

Statistical tools

(12,300 Cases)

Semi-structured Interviews

Case study Analysis

Persona

creation

ERP Scan

Research Tool Kit

Research Outcome

Maximising conciliation rate which further contribute to the revenue growth of SAMA.

Creation of a better and effective justice system through SAMA

Research Objective

Identifying dependency factors which influence a loan defaulter to do settlement.

Identifying types of defaulters and measuring and comparing the willingness to conciliate.

Recommendations for areas of intervention for SAMA to increase the conciliation rate

Defaulter often fail to recognise the future impact of the non-payment of their loans

Defaulters often carry a childish-revenge mentality when it comes to repayment.

The type of loan taken has a huge impact on the willingness to conciliate (collateral & non-collateral)

Creating a sense of equality in the defaulter’s mind is key to their willingness to conciliate

Key findings

Research Pipeline

W1

W2

W3

W4

W5

W6

Understanding Landscape

Literature review

Planning

Understanding Landscape

Literature review

Investigating Problem area

Define Problem

Definition

Design Research Funnel

Primary research

Exploration

Creating and validation hypothesis

Analysis of the data collected

Evaluation

Insights, Overall Themes,

Recommendation

Direction

Conciliation

Who is a conciliator?

A conciliator is typically a neutral third party who is skilled in conflict resolution and has expertise in the specific area of the dispute.

Impartial

Objectivity

Fairness

Expert in subject

Suitable for a variety of complexity of cases- flexibility

Creative ways of resolution

Involvement of main parties and not just lawyer

Cost-effective

Key Factors

Mutually advantageous decision-making

Quicker resolution

Privacy with confidentiality

Considers REASONS OF THE DEFAULTER leading to default

Leverage personal vindication (desire to clear reputation)

The ADR Continuum

The What,Why, Who and how?

PHASE 1 | Understanding the world of financial legislation

Neutral arbitrator renders a decision called an award, after there has been a presentation of Evidence

Occurs directly between the parties and their counsel

Does not involve a neutral third-party

Flexible process that can be used any time of dispute

Traditional method

Final verdict through court proceedings

Formal

Arbitration

Conciliation

Litigation

Negotiation

Mediation

Informal

Parties decide outcome

Neutral decide outcome

Key Objectives of Arbitration Act

People in India believed in resolving disputes within the four walls to protect their dignity and personality

In 1899 The Indian Arbitration Act, 1899 was enacted to give effect to alternate dispute mechanism in India.

Muslim rule bought in Hedaya as mentioned in Khuran

Sarpanch in Grama Panchayat

Bhradarnayaka Upanishad

mentioning about - Kula

Alternate ways - History

*What is

Alternate Dispute Resolution (ADR) encompasses various methods for resolving legal conflicts outside of formal court proceedings.It has been an important mechanism for resolving disputes in India since ancient times. ADR done online is Online Dispute reolution

Alternate

Resolution

Dispute

Less personal as the parties aren't in the same room - most conversation in writing

All parties require access to adequate technology to fully partcipate

Parties with difficulty in language in writing may be at disadvantage

ODR is a non-binding process, it cannot produce legal precedents

Disadvantages

Weaker party less likely to trust ADR

Likely to be biased as the lenders approach neutral party

Reaching agreement makes the party feel smaller and weaker

Big stakes cases cant be solved through ADR

Myths and Assumptions

*Why a need for

Alternate

Dispute

Resolution?

35L

cheque bouncing cases pending in courts across India

32M

million cases pending across courts in India- post-lockdown

90%

financial cases can be resolved without the engagement of a judge or mediator

10L

crore

loans written off by in last five financial years

**Non-performing Assets is a loan or an advance for which the principal or interest payment has remained overdue for a period of 90 days.

5%

Gross **Non-performing assets ratio of India is a 7 year low

REACH AN AGREEMENT

GET A DECISION

*Who is

SAMA

SAMA's goal is to give you a safe, quick, cost-effective and humane approach to resolve your dispute to your satisfaction with real practical solutions without the expense or hassle of courts and spending a lot of time.

Creation of a new justice system with the integration of technology through collaboration to increase effectiveness

Suljao Magar pyaar se

VISION

MISSION

*How

SAMA

works

Statistics

SAMA

USER PROCESS FLOW

Quantitative Data Analysis

(12,300 Cases)

Semi-structured Interviews

Case study Analysis

Persona

creation

ERP Scan

Research Tool Kit

Locus-of-control

People with internal LoC are twice more likely to save for the future than people with external LoC.

Other factors

Attitude towards Debt

Greed

Time Preference for money

Social Stigma

Self-esteem

Personality

It affect the credit risk of borrowers, the response pattern differs significantly in high stakes and low stakes settings.

Integrity

Borrowers with low integrity may opt to default.

Borrowers’ ability (Can be predicted)to repay and Borrowers’ willingness isnt captured as of now by the system

Impulsive/compulsive buying

Lack of self-control represents delinquency in repayments and financial distress.

Materialism

Individuals who believe that possession of goods will lead to success have low debt and high account balances.

Self-Efficacy

Some researchers have indicated self-efficacy as a positive aspect of a borrower, others have related it with overconfidence and a higher degree of optimism.

Understanding defaulter mind set

Creation of Inclusive rights

Research Approach Funnel

Data Analysis- Quantitative & Qualitative

Hypothesis Creation and testing

Secondary Research

Stakeholder Interviews

Debt Recovery tribunal Visit

Hypothesis Validation

Quantitative Data Analysis

Hypothesis Creation

Data Cleaning

Descriptive Analysis

Statistical Analysis

Data Synthesis

Data Sampling

Stakeholder Interviews

Quantitative

Qualitative

Validation

PHASE 2 I PRIMARY RESEARCH

How might we improve the process of conciliation as an alternate dispute resolution method to tackle loan default cases.

Problem Statement

Maximising conciliation rate which further contributes to the revenue growth of SAMA.

Creation of a better and more effective justice system through SAMA

Defaulter centric

insights

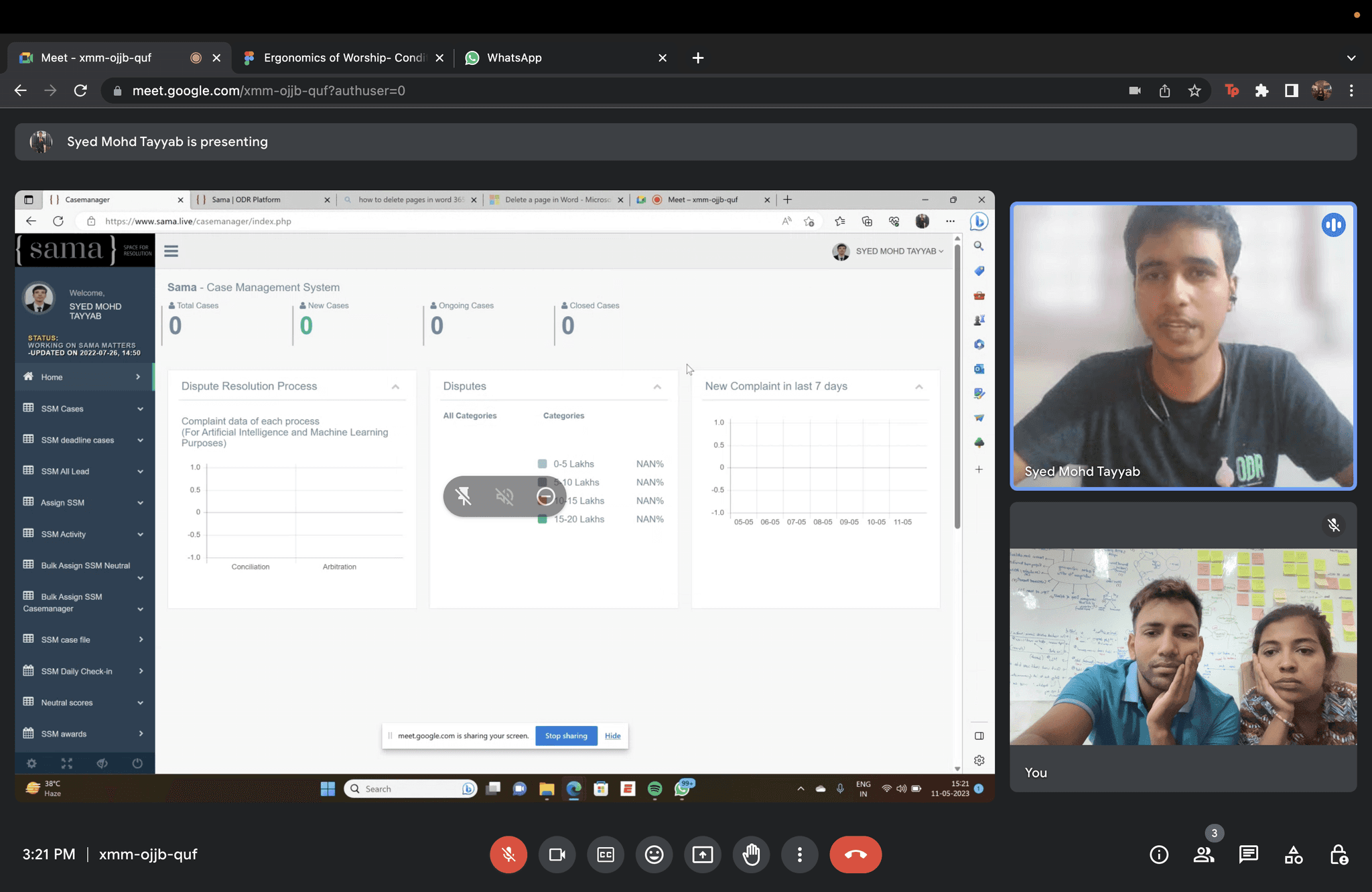

SAMA internal data

Sangeetha Mehrotra

Conciliator, SAMA

Case managers & conciliators (within SAMA)-12

Conciliators outside SAMA -5

Debt service expert interview

Defaulter interview - 15

Interviewee pool

"Defaulters often mistake us as collection agents"

"They don't know that we are here to listen to their problems"

Awareness

Lack of awareness about the consequences of willfully defaulting

Lack of realisation that compromises are made by both the parties

Lack of awareness about financial discipline leading to NPA

The shame associated with the default blurs the line between willingness vs. ability to settl;e

Defaulter Behvaiour/insights

Very less number of female defaulters- women are the poc in defaults made by the men

Human nature to argue during conflicts drip down to ADR

Childish revenue mentality by defaulter- I lose, you lose

Willingness to conciliate

=

Willingness to pay back

Use ADR to delay litigation process

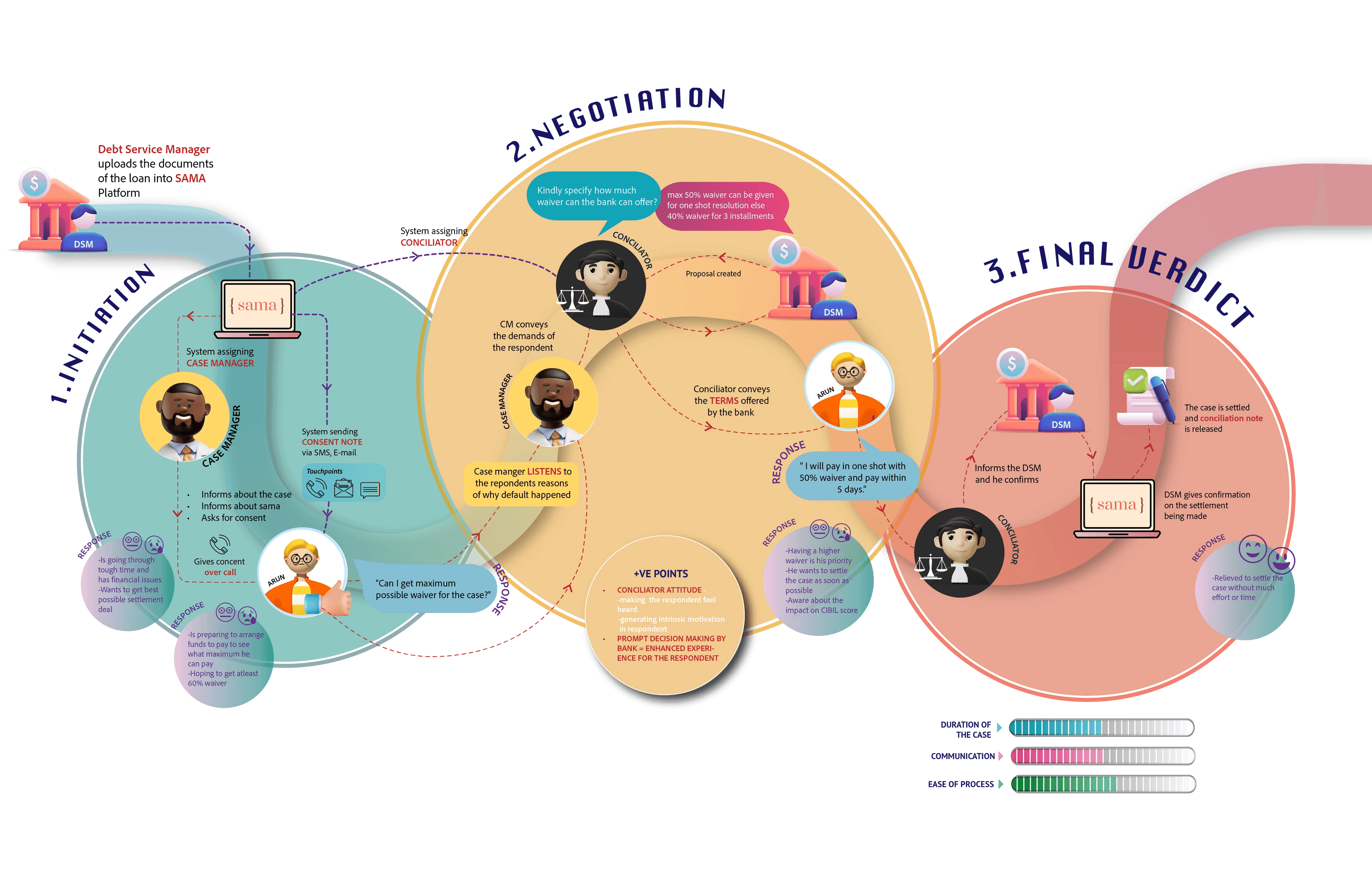

"After conversations in the initial 10 min, I can figure out, saying/doing what would want to make them settle. Sometimes they seek a listener of their problems and sometimes I become the teacher who scolded a kid"

SAMA- Operations

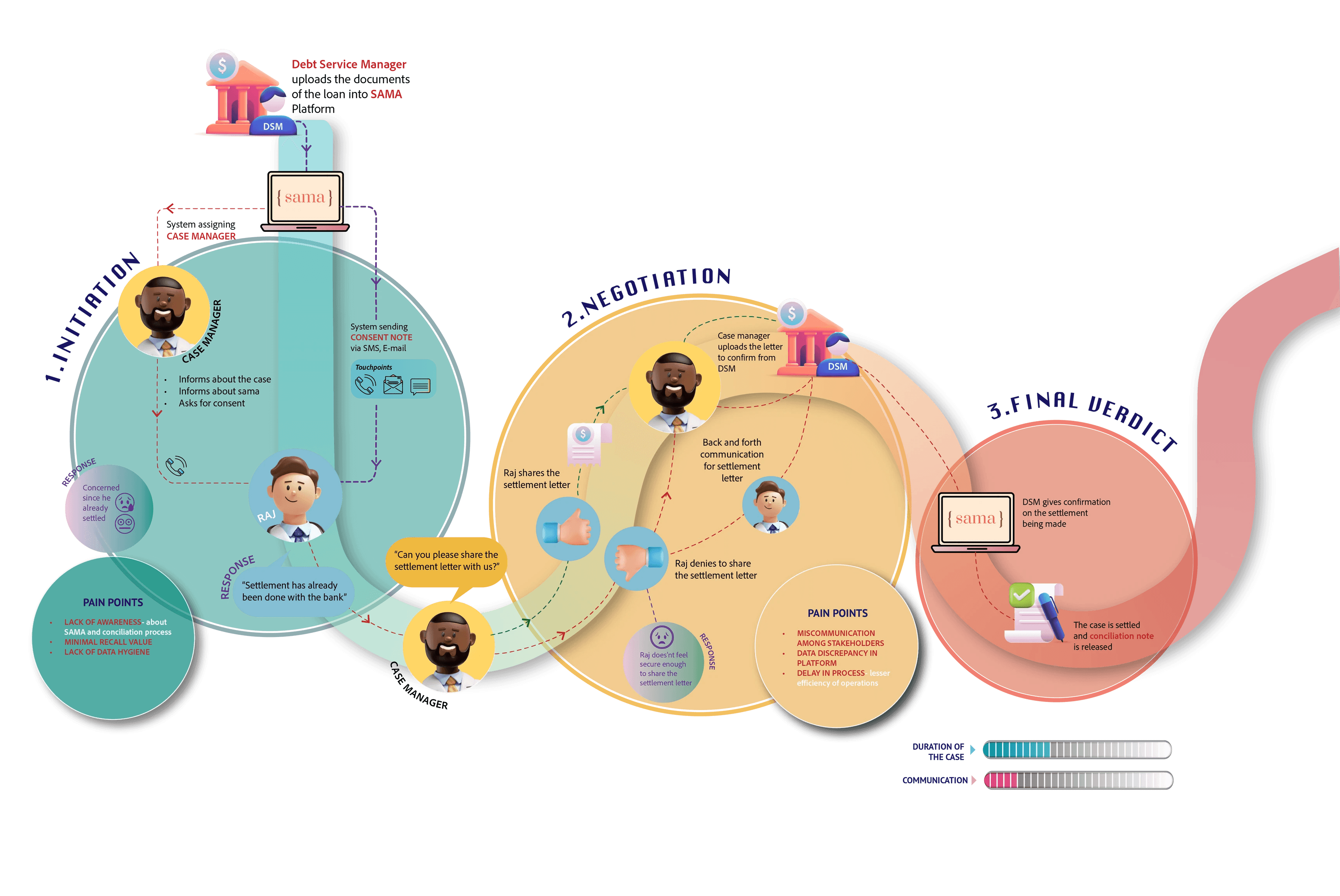

Lack of Data Hygiene from the clients- leading to incomplete data in SAMA-ERP

Case Managers playing role of neutrals and vice vers

Multiple stakeholders- Bank, Collection agent and SAMA- are approaching the defaulter at same time

Informality is triggered as conciliation consent notices arent digital

Lack of enforceability as Litigation is ahead if methods of ADR didn't work out

Failure to pick up habitual cues as contact isn't physical rather than. virtual

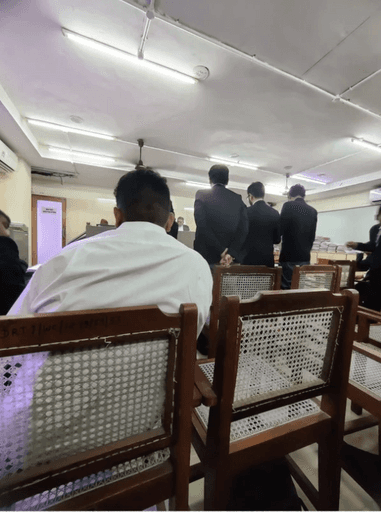

Debt-Recovery Tribunal | Court visit | Highlights

Lack of empathy

Debt recovery Tribunal is the exclusive court which handles disputes regrading Debt defaults. This visit was conducted to grasp concepts of traditional litigation-what to leverage in creating an effective justice system

One sides conversation from judge to defaultees and lenders

Most cases have been going for years

All stakeholders focused on getting the next hearing date

most of the cases didn't have the borrower present-still verdict was issued

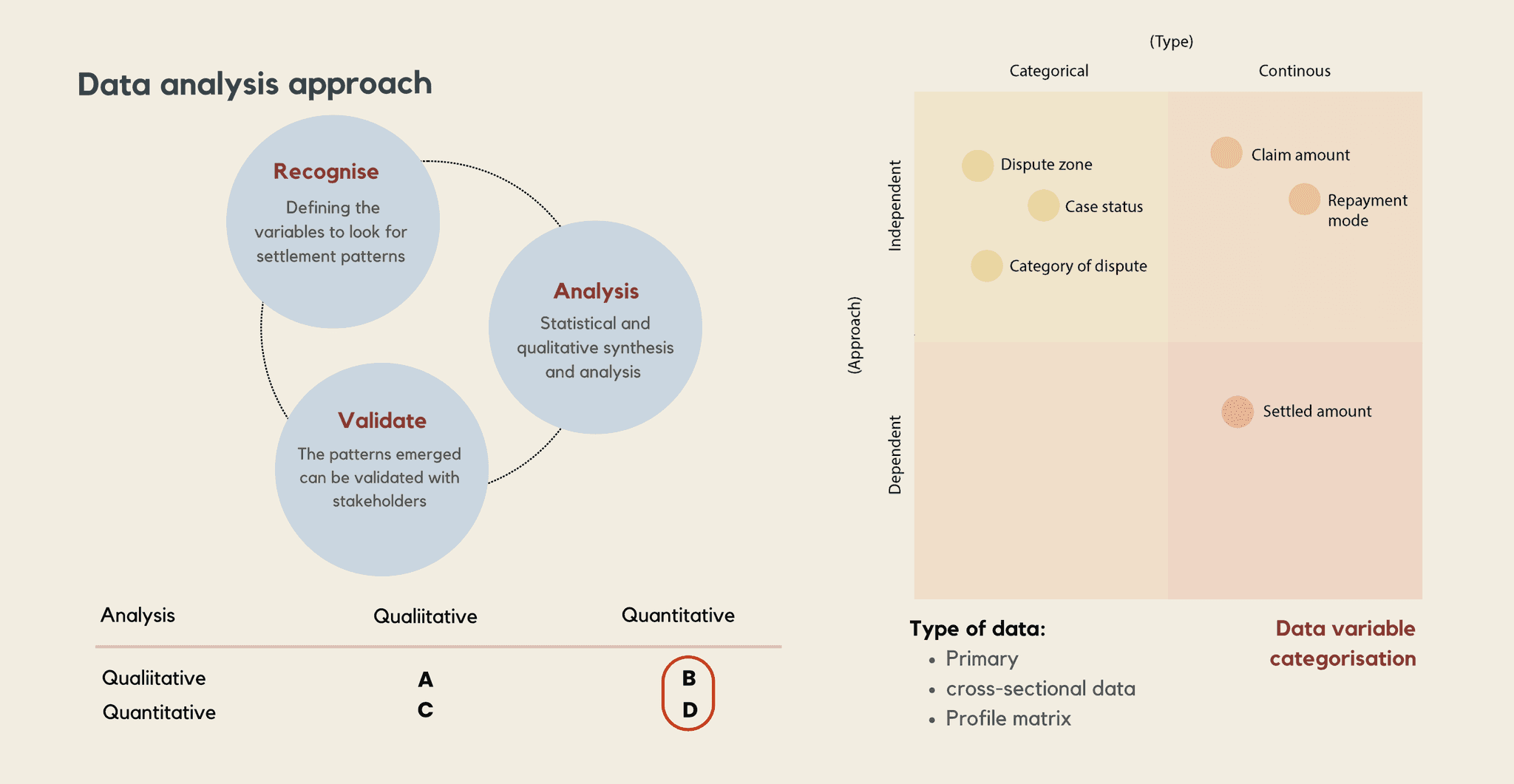

Data Analysis Approach

Hypothesis Creation and testing

Data Analysis- Quantitative & Qualitative

The Data variables to cross compare and analyse was identifies by us post the secondary and primary research

To uncover the external and internal factors affecting the settlement beahaviour, quantitative data was looked at multiple angles

ANOVA

Conducting analysis of variance to determine the differences in settled amount across independent variable

Cluster Analysis

identify groups of loan default who exhibit similar behaviour

Correlation Analysis & Chi-square test

To quantify linear relationship between pair of various variables

Statistical tools explored

Semi-structured Interviews| ERP Scan | Highlights

12,304

Total cases studied

9706

Credit card cases

3%

Current conciliation rate

2603

Personal loan cases

155

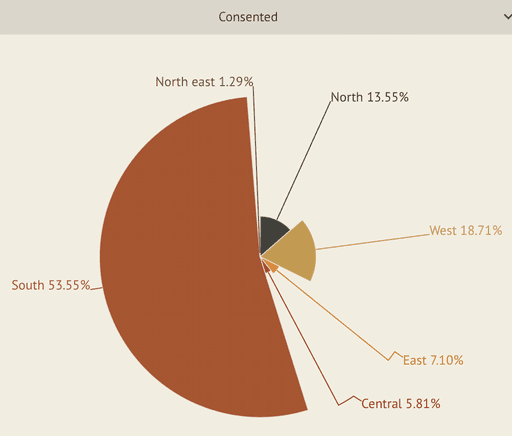

Consented

187

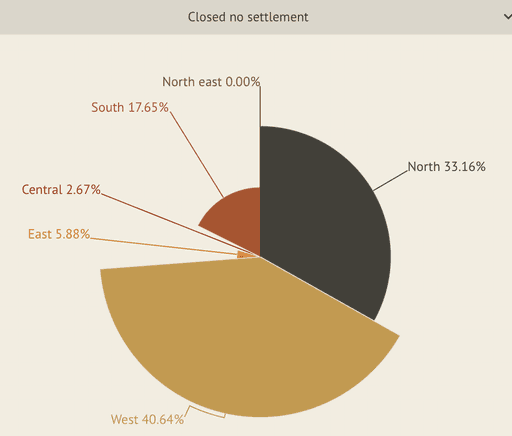

Closed no Settlement

361

Settled

Data

Statistics

Descriptive Analysis

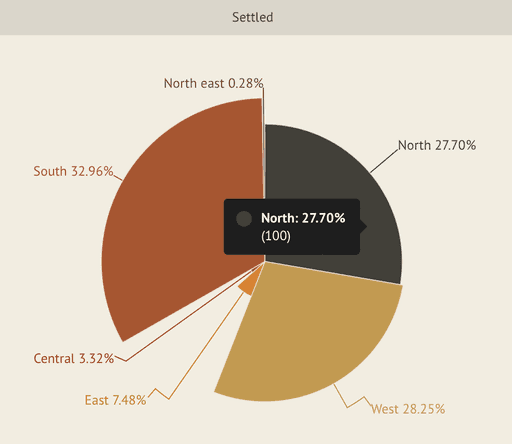

Demographical breakdown

The high consented rate from South India is attributed to the top-performing debt service managers- who are handling cases in the south region

Managers highlighted defaulters from south were more responsive in the first call.

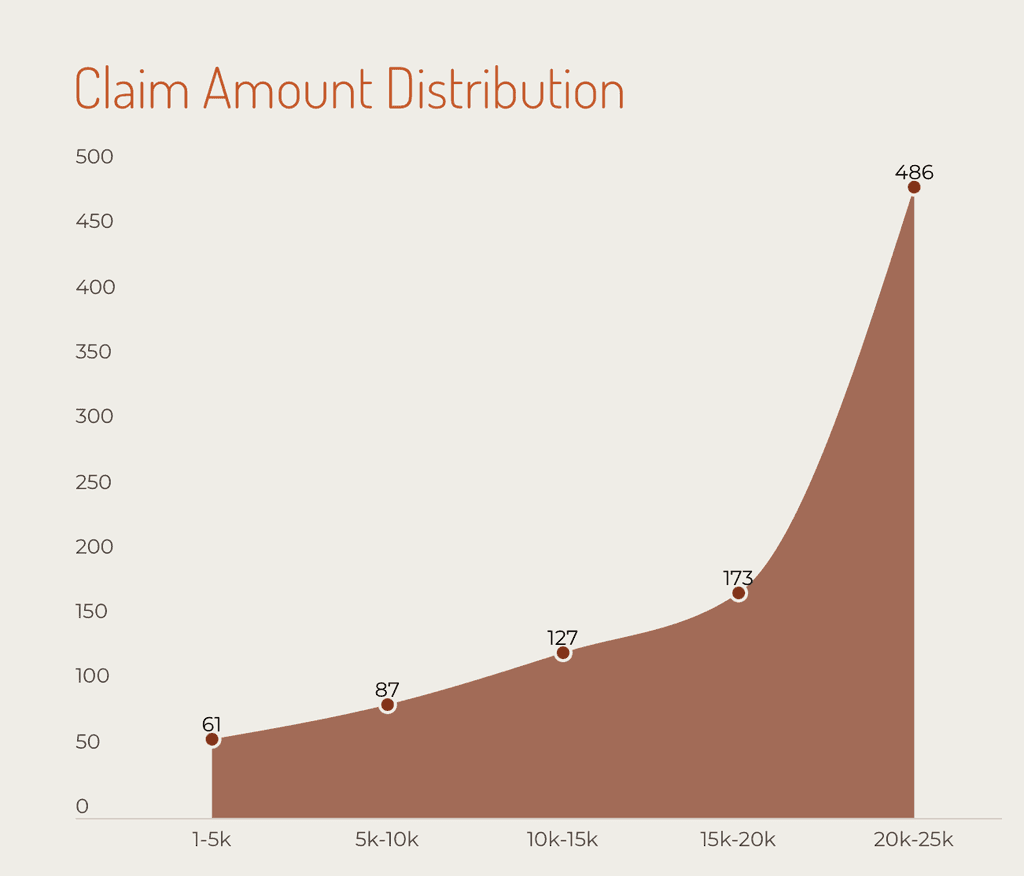

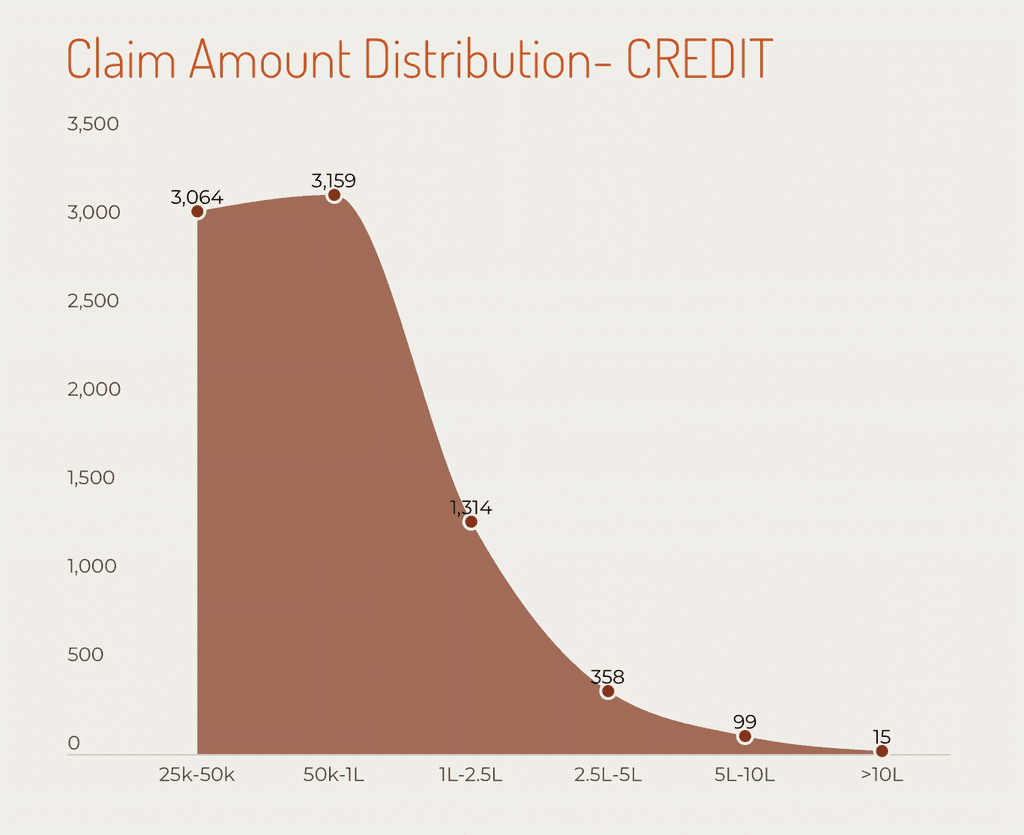

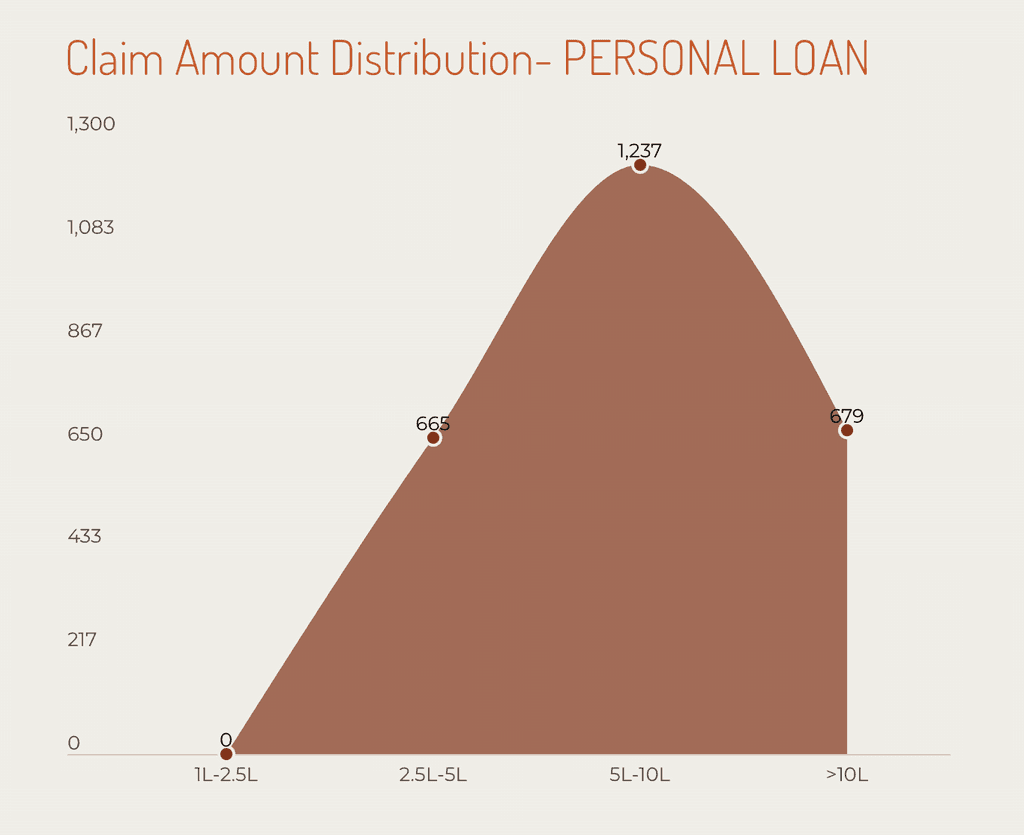

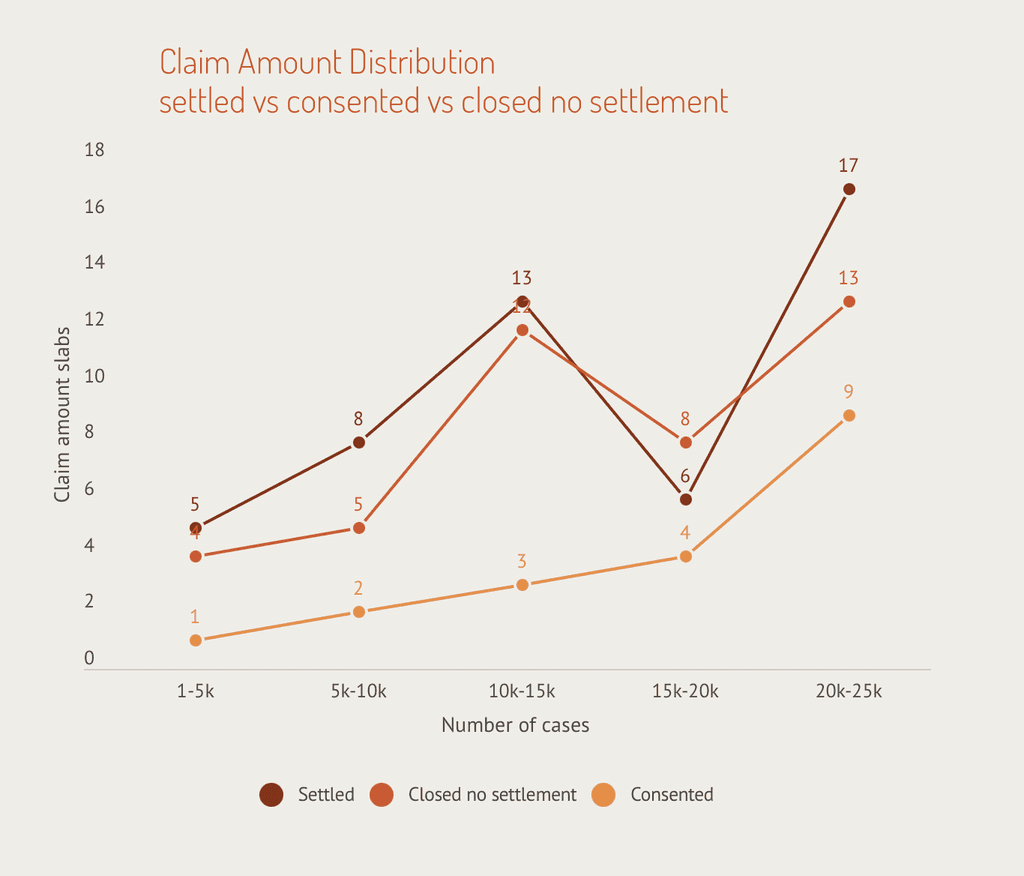

Amount Distribution

Settled cases are highest in high claim amount cases

Consented cases(said yes to conciliation isn't moving further) seemed to be present across all claim amounts- reasons pointed towards internal operations

Co-relation Analysis

Type of loans have an impact on the willingness to settle

Linear Co-relation

HIgher claim amount- Higher the settlement amount

Disproven

We believe that

Objective Hypothesis Creation

Loan defaulters with higher claim amount have more chances to consenting to conciliation

We believe that

Approach to settlement is loan category dependent

We believe that

Delay in processes and operation is leading to lesser chances for the case to get settled through conciliation

We believe that

Approach to settlement is loan amount dependent

We believe that

SAMA act as a nudge for the respondent if he was already planning to settle.

We believe that

Respondents look at conciliation as. a casual process hence conciliation rate is affected

We believe that

Data discrepancy in the portal leads to fallout of respondents post consent

We believe that

Respondents are not feeling secure enough to share their docs with SAMA

We believe that

CiBIL score have an impact on the willingness to settle through conciliation

Disproven

Disproven

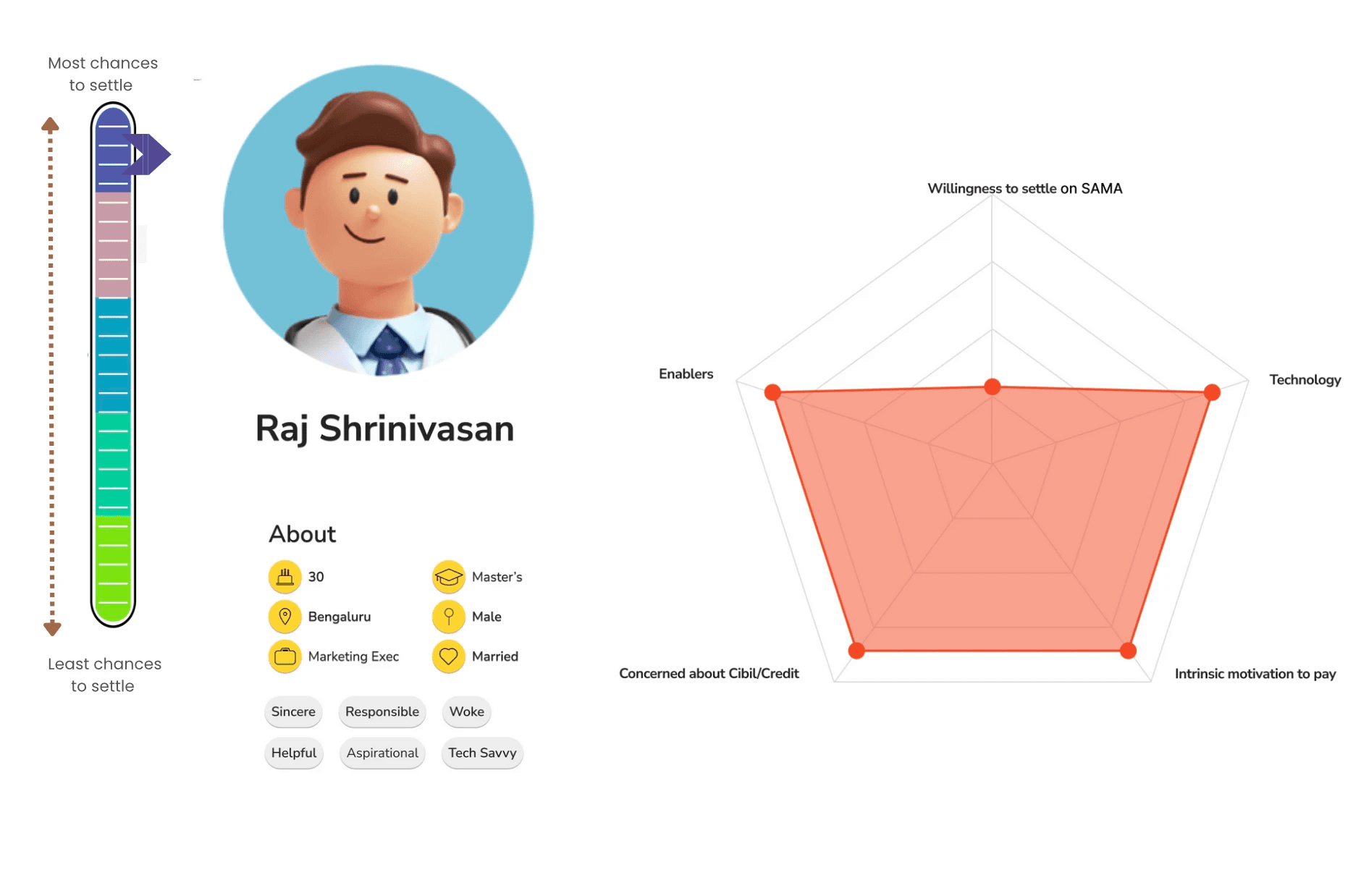

Willingness- to- conciliate meter

PHASE 2 | Primary research

Willingness -Conciliate-Scale

PHASE 3 | DATA ANALYSIS

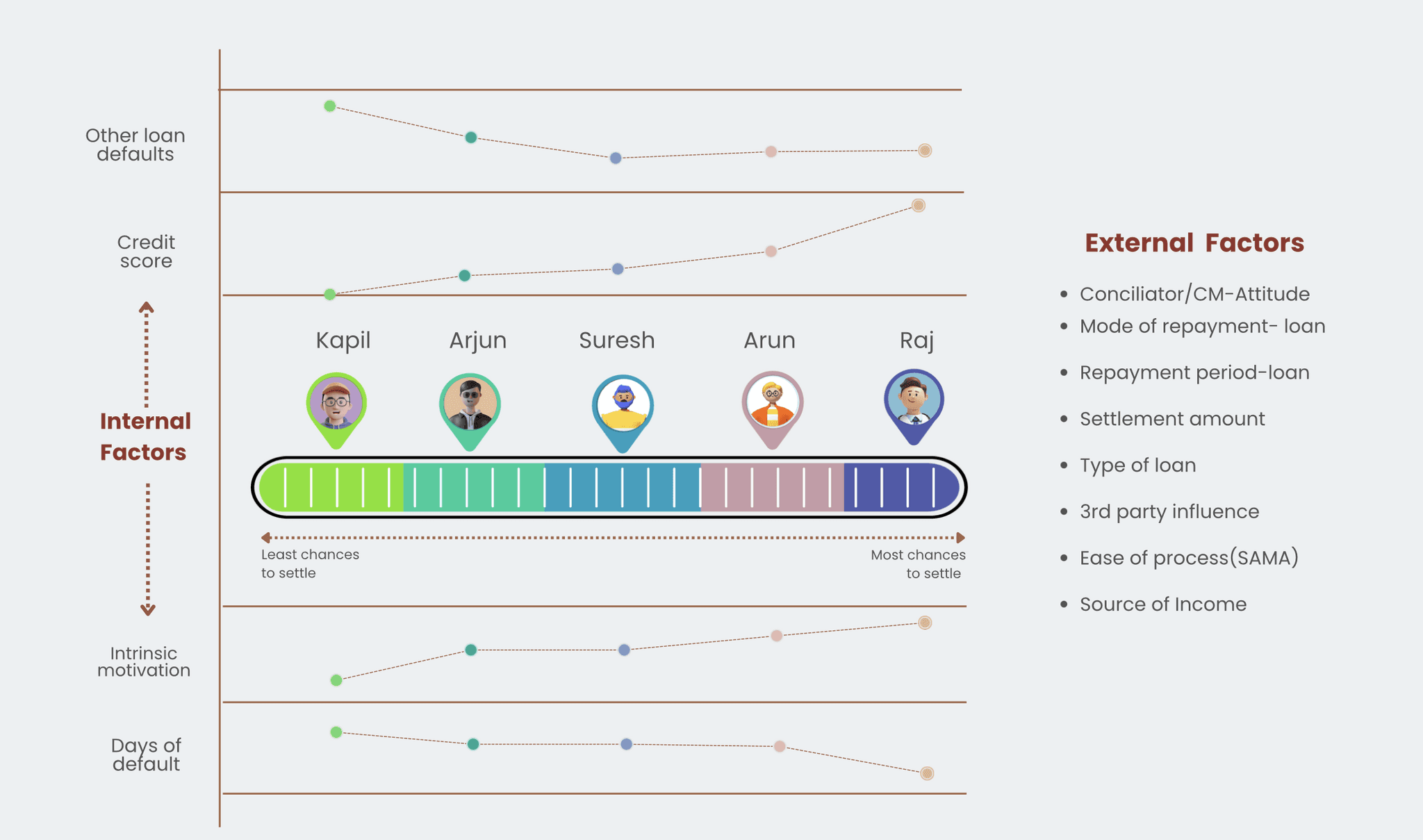

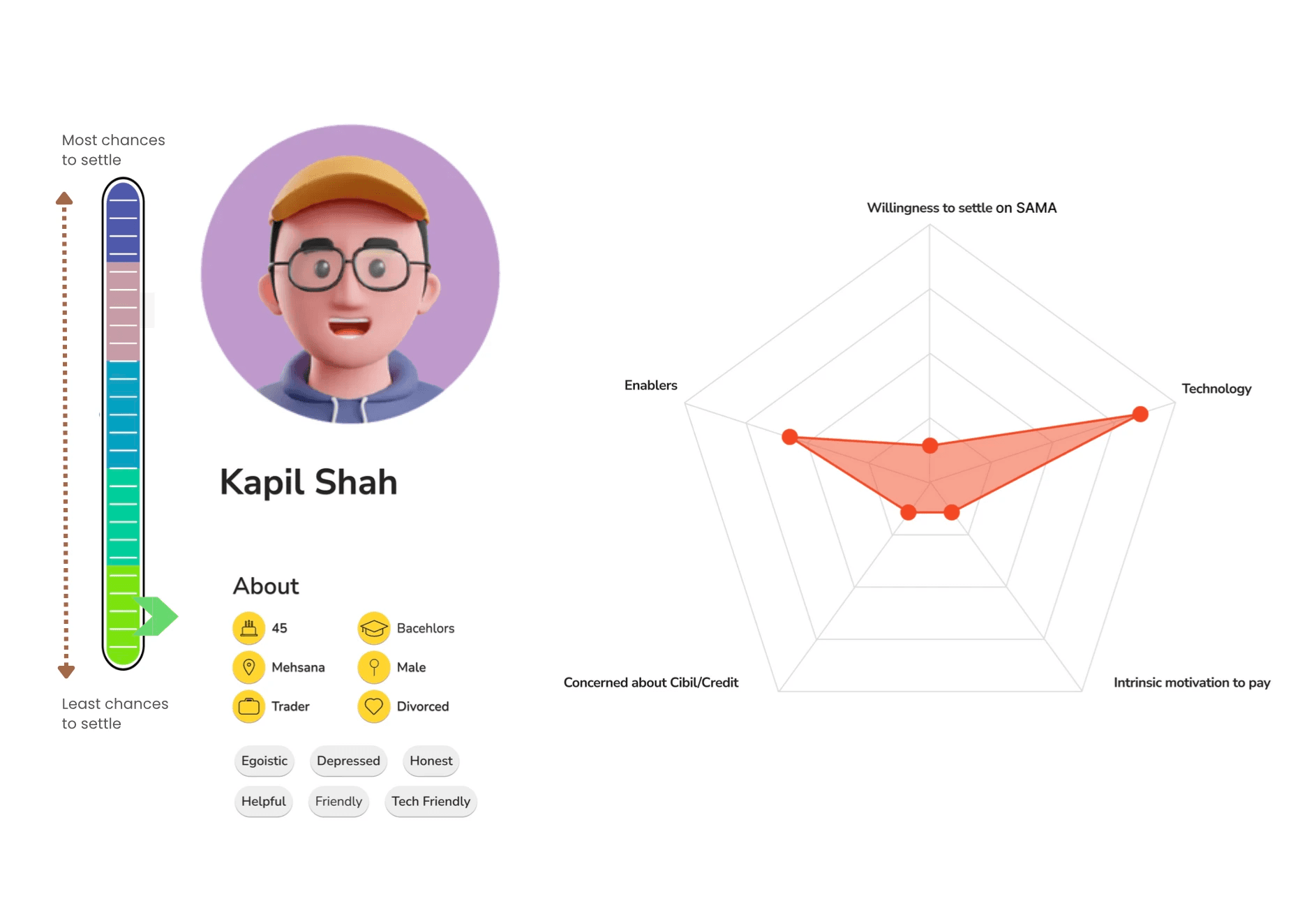

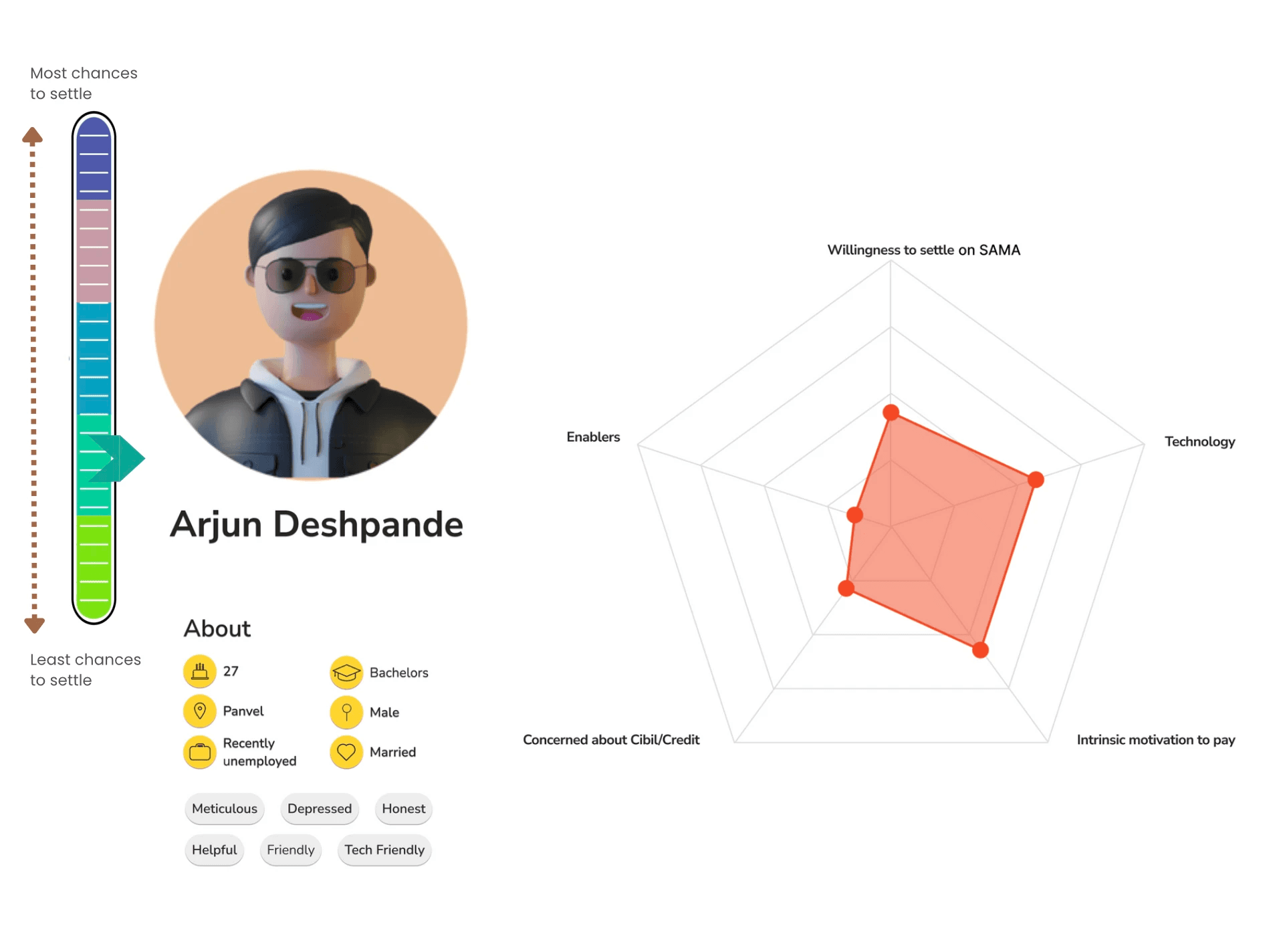

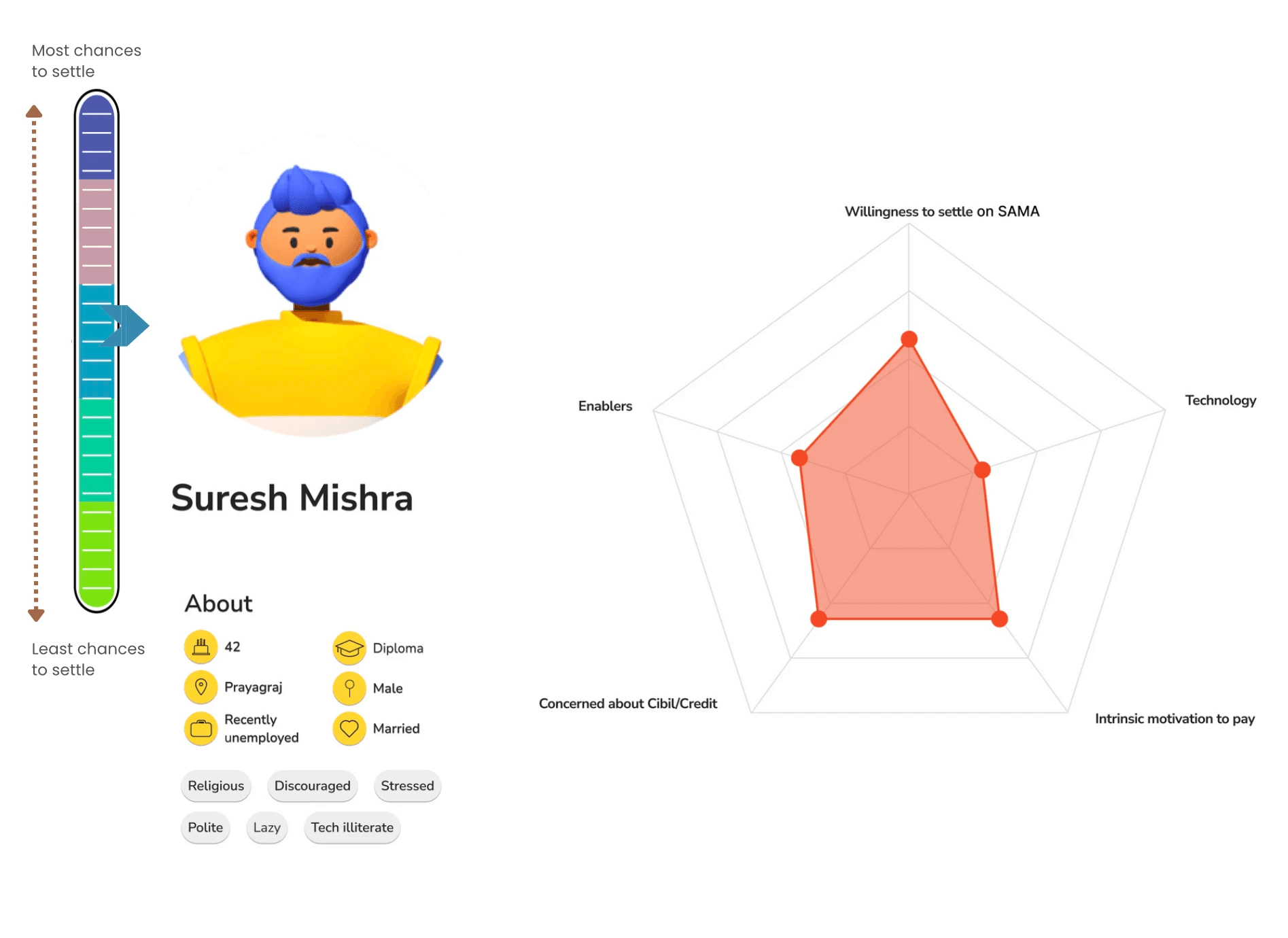

Persona 5

Factors influencing his willingness to settle

Ego

Attitude of bank

CASE SCENARIO 5

Factors influencing his willingness to settle

Credit/CIBIL Score

Source of income

Personal issues-medical,finance

Consequence of default

Previous loan default

Other loans

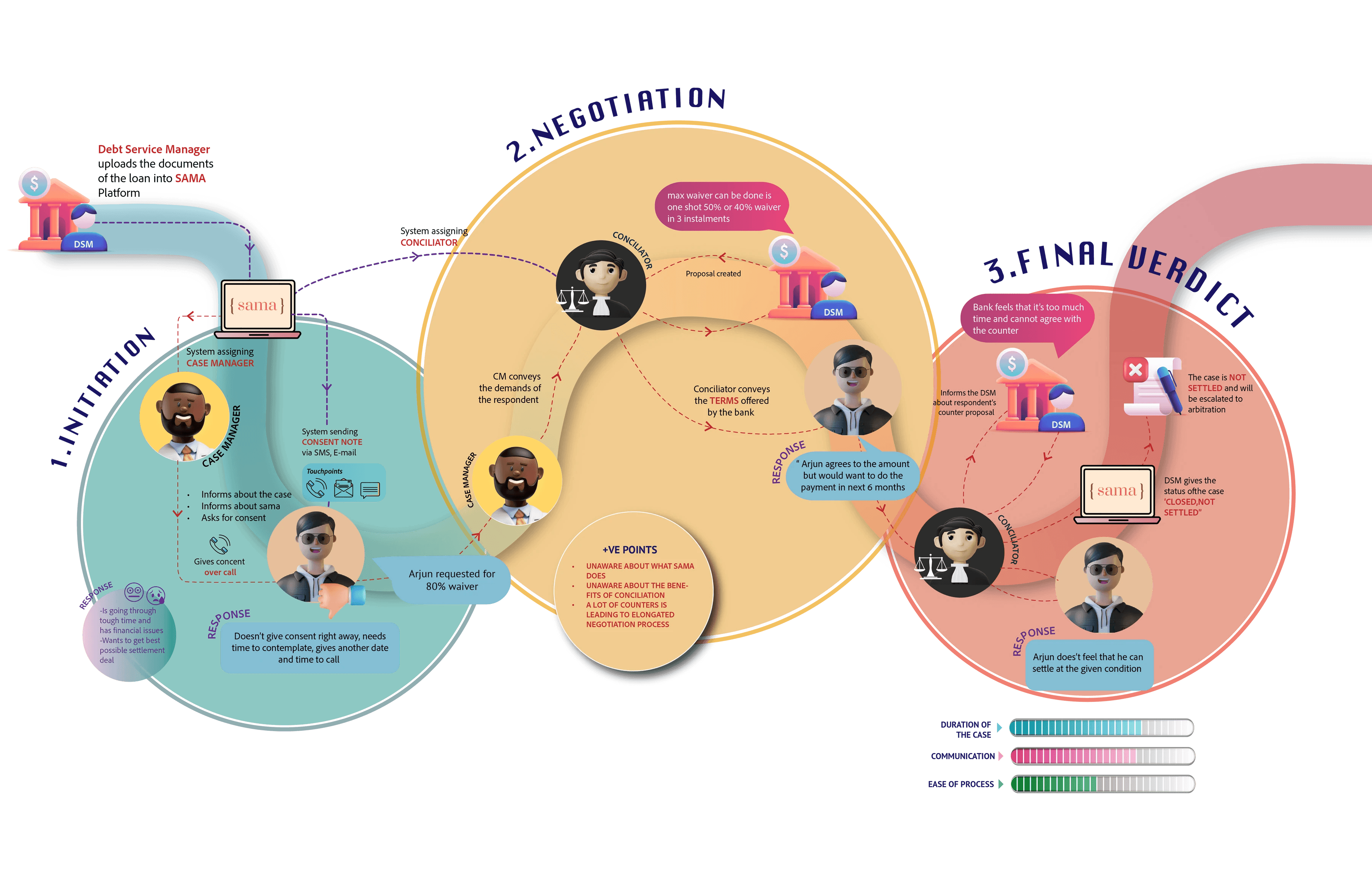

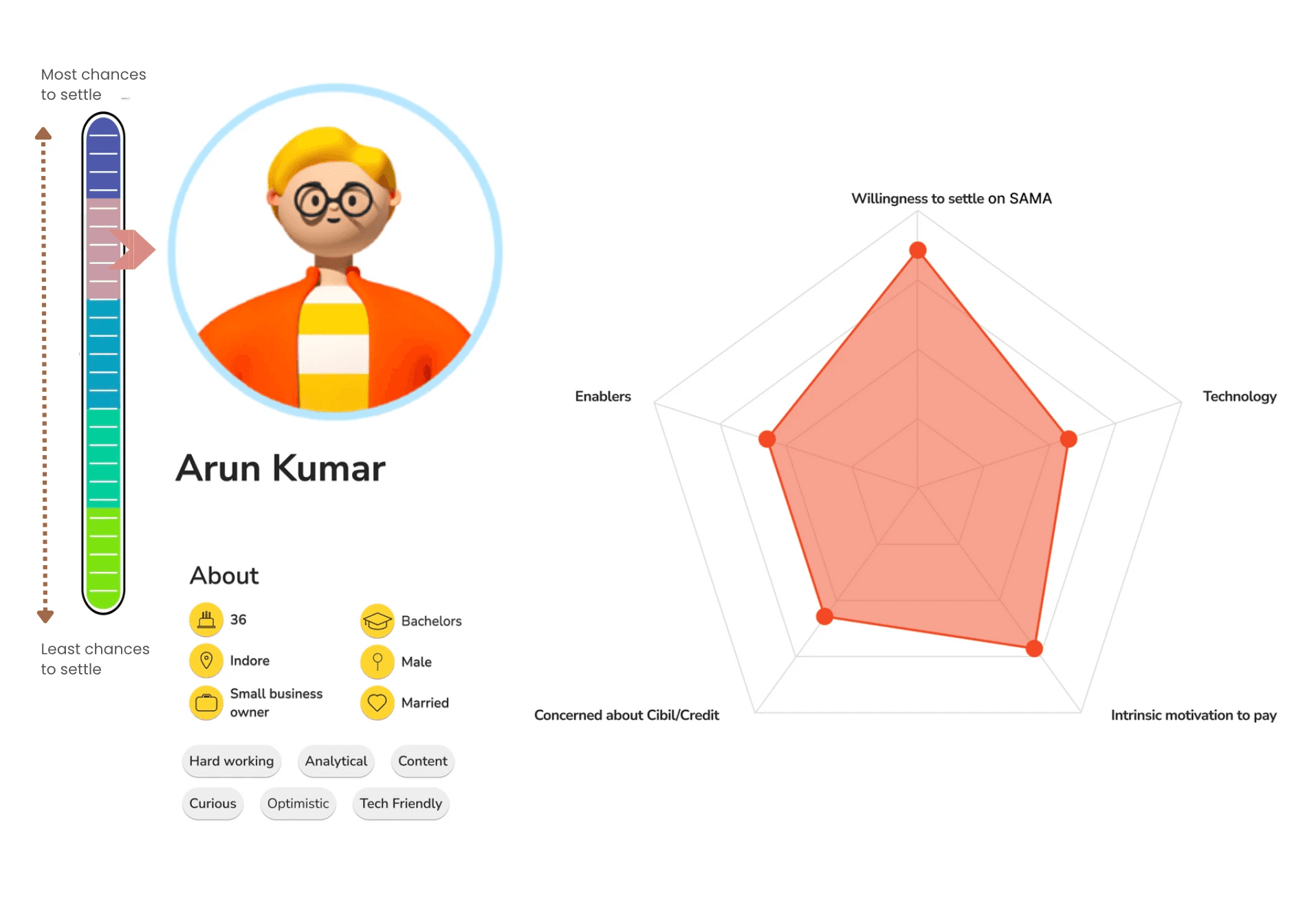

CASE SCENARIO 4

Persona 4

CASE SCENARIO 3

Factors influencing his willingness to settle

Credit/CIBIL Score

Source of income

Personal issues-medical,finance

Consequence of default

Previous loan default

Other loans

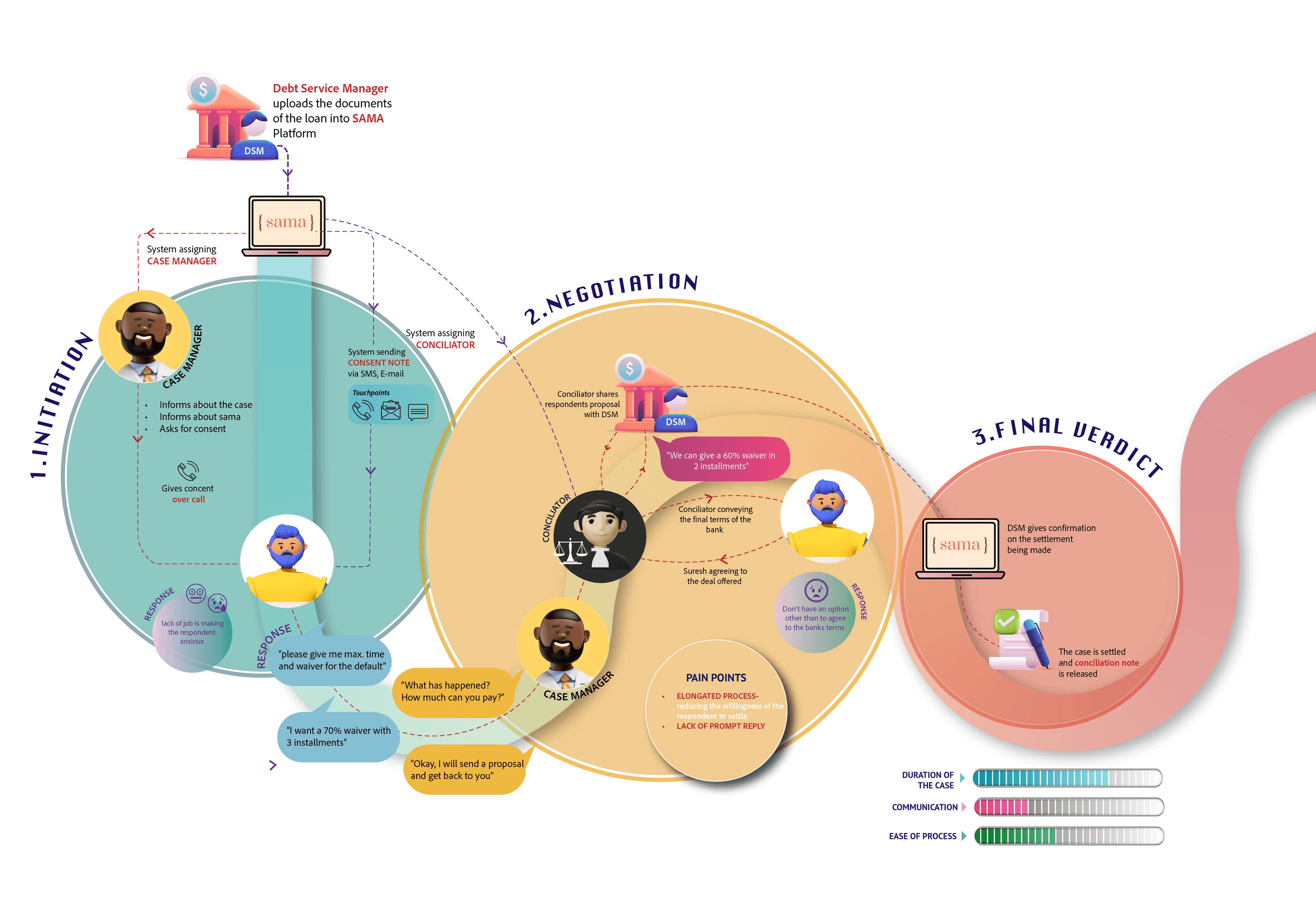

Persona 3

CASE SCENARIO 2

Persona 2

Factors influencing his willingness to settle

Credit/CIBIL Score

Source of income

Personal issues-medical,finance

Consequence of default

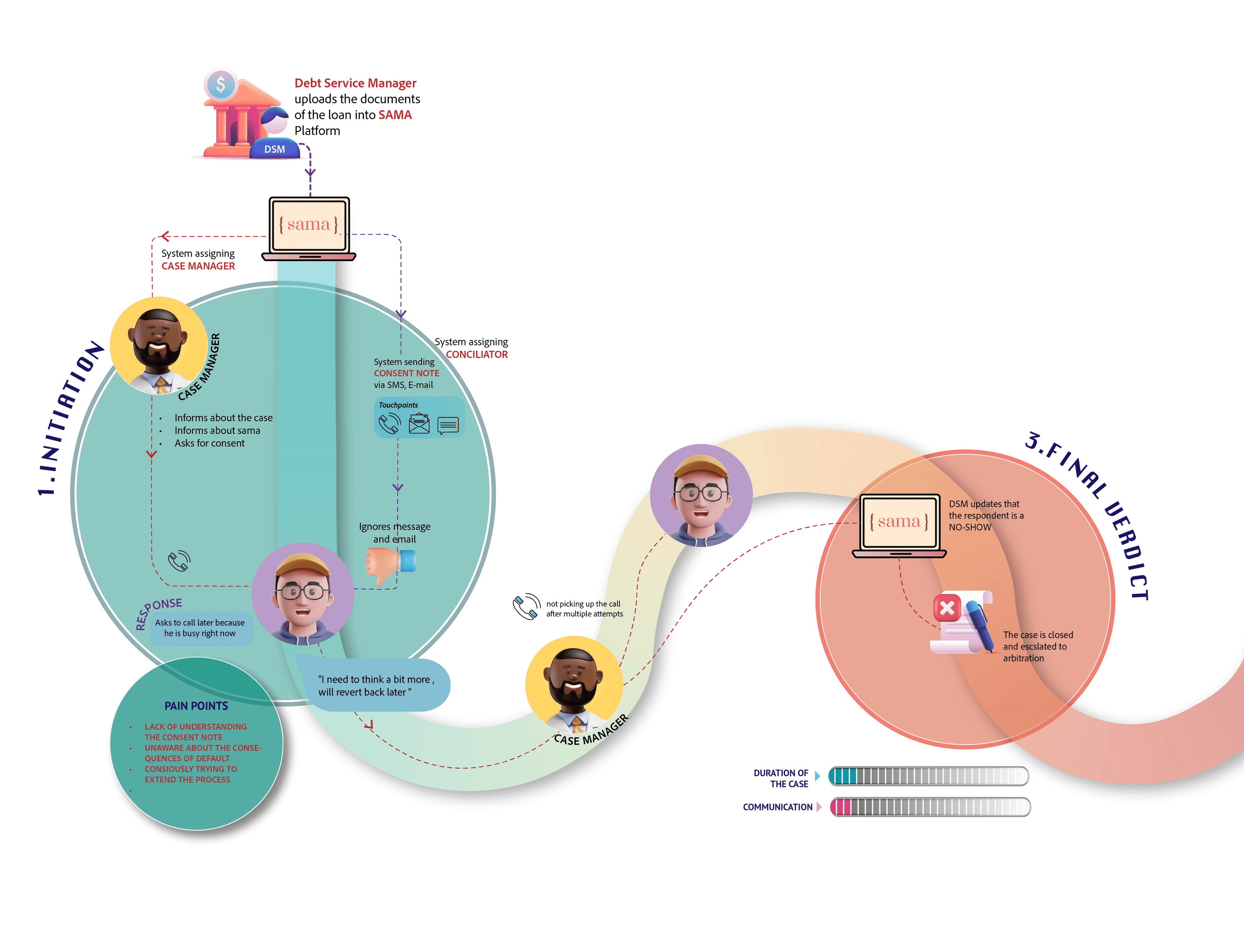

CASE SCENARIO 1

Factors influencing his willingness to settle

Credit/CIBIL Score

Source of income

Persona 1

Case scenario Analysis & persona creation

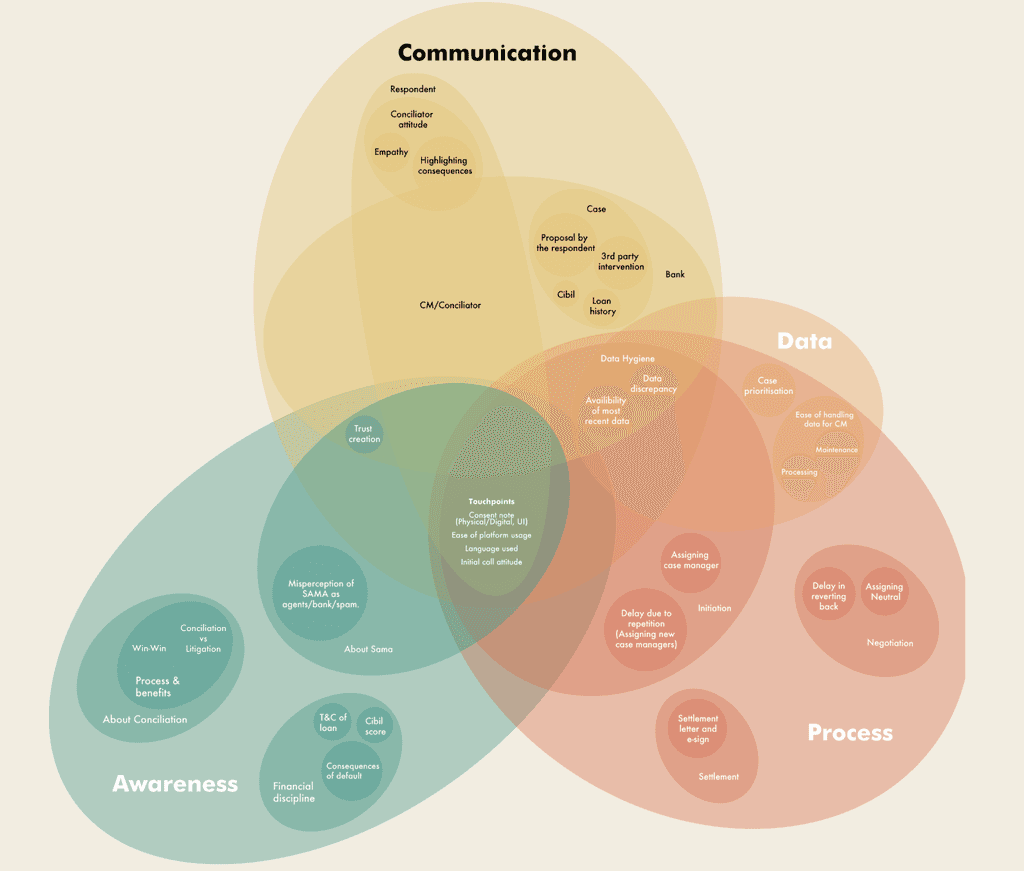

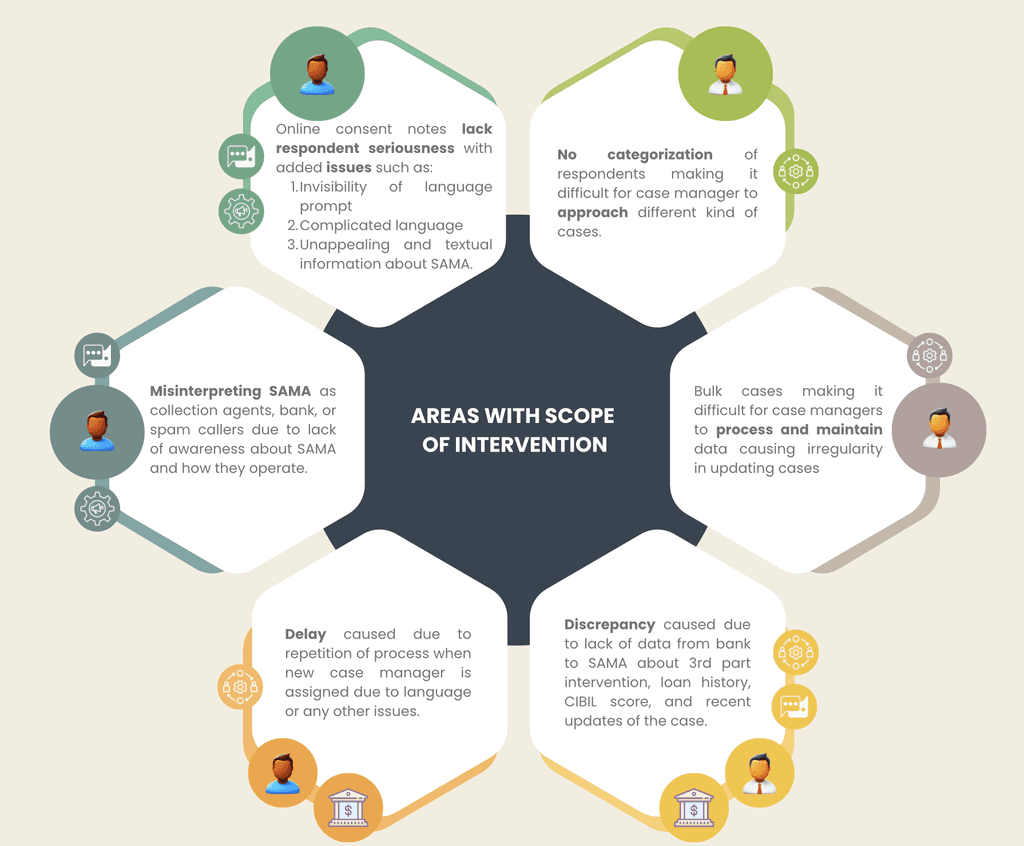

Data Hygiene issues/data discrepancies internally and bank level

Availability of most recent data to case managers- ease of handling data Initiation stage issues

Delay in the process while assigning case managers

Manual assigning of case managers which causes repetition

Lack of case prioritization

Negotiation stage issues- DSM's causing delay in reverting back

Data & Process

Sama has a minimal recall value based on the calls that we made.

3rd party intervention confusing users.

There is a considerable delay in communication on the platform in regard to the stakeholders like DSM and Case managers which extends the case timeline

The Language tab on the consent note is non accesible and the overall UI and the language of the consent letter can be much simpler.

SAMA needs to be in a position to demand the following set of data from the bank as a must- Previous loan history, any third party intervention, CIBIL score.

The peace note and the consent letter to go physically to build the aspect of informal but not casual.

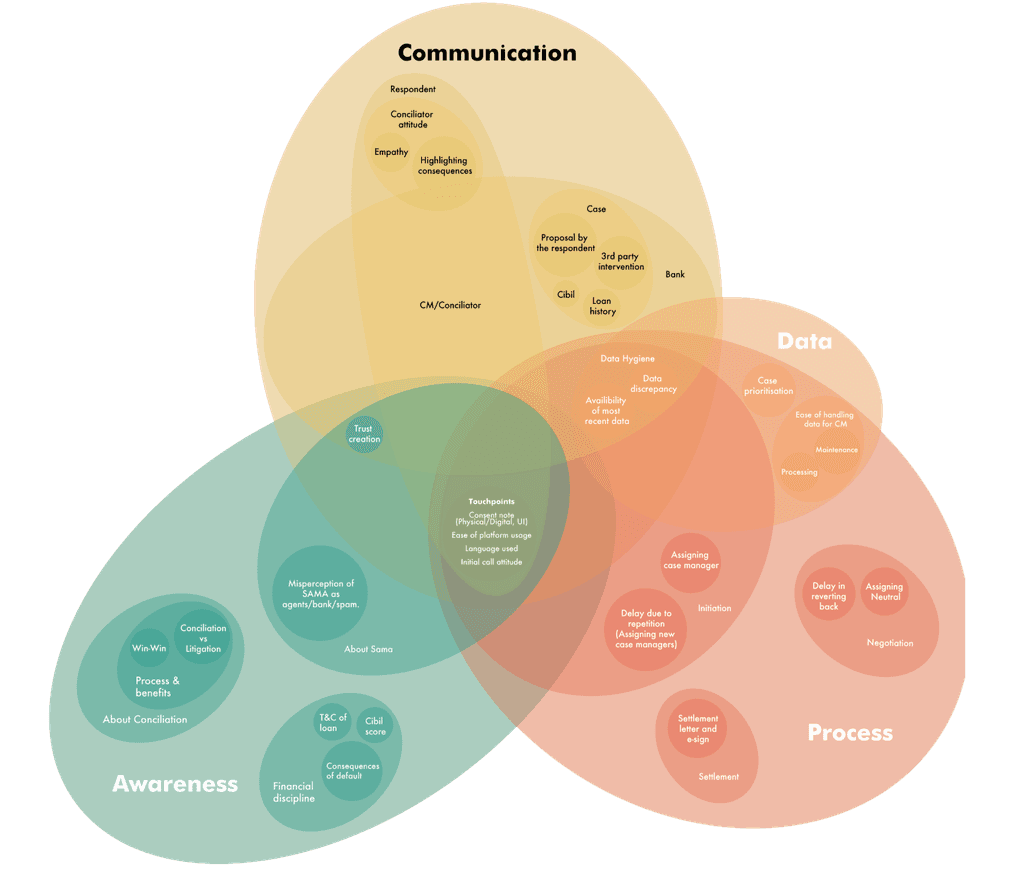

Communication

Lack of awareness about conciliation- process of conciliation and it benefits, only gets to know from the initial call.

Aren't truly aware that it is a win-win situation

Lack of awareness about SAMA and hence misperception of SAMA being collection agent/bank/spam.

On a system level, lack of awareness about financial discipline, about consequences of default, affect on civil score, and terms and conditions of loan.

Awareness

Theme Map

Areas of Intervention

Direction Ahead

Consent letter

- Conciliation has to be informal but not casual

- A peace notice, along with the consent letter in the regional language to be sent physically to tackle that.

- Setting the tone for SAMA as a help not a collection agency or bank representative and creating trust.

Case Manager- Guide book

- Willingness to settle meter

- Type of loan

- CIBIL score

- Loan amount buckets

Nudges & Notifications

- Automated nudges on the platform that remind case managers to take updates for any pending cases in their pipeline.

- Highlight summary of total cases pending to CMs and segregation according to amount buckets, and case status currently only available in God mode.

Internal communication

For better communication between the case managers and respondent, SAMA need to seek the following data from the bank

Days of default

Previous communication of respondents with other stakeholders

Availability of most recent data

Theme

Identification